Credit score. You’ve heard of it. But what is it, and why is it important for buying a house? Your credit score gives lenders an idea of how likely you are to make your payments on time. Depending on the model, credit scores typically range between 300 and 850. Higher credit scores sometimes lead to more favorable loan terms, whereas lower credit scores (below 620, for example) may have more restrictive loan terms and higher interest rates. While many factors go into determining your credit score, lenders consider it a pretty good snapshot of your financial health and history.

Equifax, Experian, and TransUnion are the three main credit reporting agencies. You can request a copy of your credit report for review directly from each bureau or go to the Fair Credit Reporting Act (FCRA) website annualcreditreport.com (opens in a new tab) where you can obtain a free credit report once every 12 months. It may also be a good idea to check your credit report regularly through each credit reporting agency, individually. By staggering when you get your credit report, you can monitor your credit throughout the year in case there are any reporting errors. If you find errors on your report, each credit reporting agency provides instructions on disputing records and getting them corrected. It is important to follow up and correct errors so that your credit report is accurate.

One helpful way to potentially improve your credit score quickly and easily is to have errors corrected or recent credit card payments reflected on your credit report through rapid rescoring. Fees may be associated with rapid rescoring so check with your lender to see if this is a no-charge service they have available. Learn more about your Credit Score and the Loan Process here.

Why Credit Score Matters

While it’s true that lenders prefer borrowers to have higher credit scores, you don’t always need a high score for homeownership to become a reality. Even with a score of 620 or lower, you may still qualify for a mortgage.

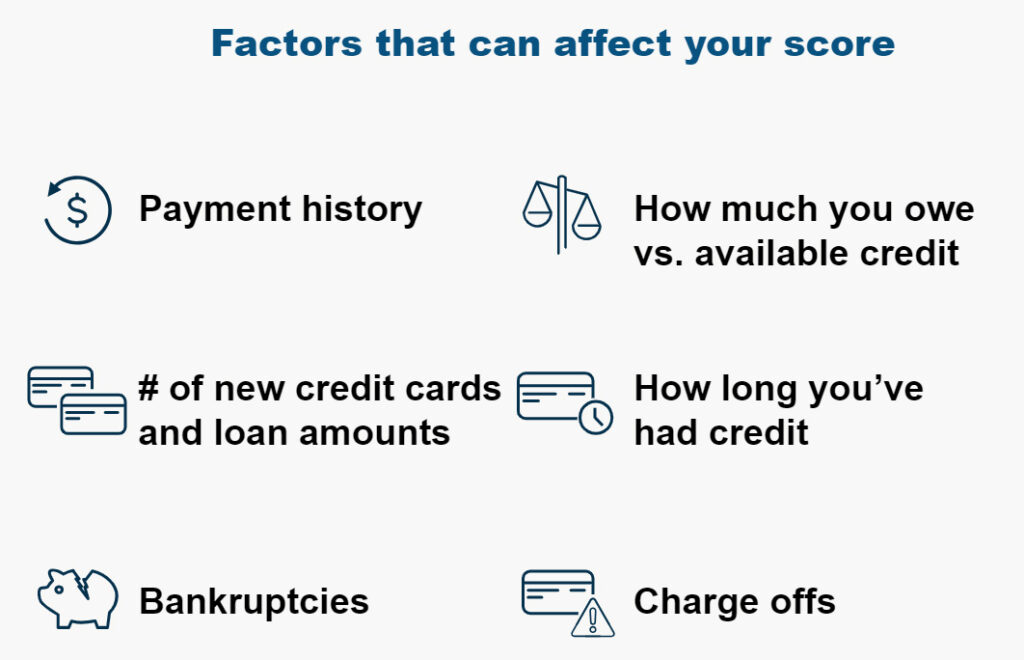

What Affects Your Score

Many factors go into your credit score. Details can be found on your credit report and include:

- Your payment history,

- How much money you owe compared to available credit,

- How long you’ve had credit,

- The different types of credit accounts you have, and

- How many new credit and loan accounts you’ve opened.

Each of these factors impacts your score differently, and the formula for figuring out your credit score differs among each of the three credit reporting agencies (Experian, Equifax, and TransUnion). Plus, if you’ve had any charge-offs or bankruptcies, these are also reflected in your score.

Know Your Credit Score

By federal law, you can obtain a free credit report once every 12 months. Alternatively, you can get three free credit reports a year—one from each credit reporting agency via the Fair Credit Reporting Act (FCRA) website annualcreditreport.com(opens in a new tab). You’ll need your address, Social Security number, birthdate, and other basic identifying pieces of information. It’s a good idea to check your credit report regularly in case there are reporting errors. As a way to monitor your credit throughout the year, you can stagger when you get your credit report from each agency. Also, many banking and credit card companies provide customers with their credit scores, free of charge.(opens in a new tab)

Credit Score and Buying a House

Purchasing a home is a big investment. This is why lenders want to make sure you’ll be able to pay it back on time, and your credit score is one of the most important indicators of this. Your lender will consider your credit score and credit history, combined with other factors such as your income in relation to your debt obligations (also known as your debt-to-income ratio, or “DTI”) and employment history, to determine your eligibility for a loan.

Improving Your Credit Score

If you’re thinking of buying a home and are concerned that your credit score is too low, you can take steps to improve it. Note that it takes time for some changes to impact your credit score, so plan ahead and get started.

Where To Begin

First, make sure there are no errors on your credit report. Double check that accounts listed and your payment history are accurate. Pay close attention to any late payments, charge-offs, collections, or closed accounts. Creditors will report these on your credit report quickly but can at times be slow to report when you’ve satisfied past-due obligations. Making sure these are accurately reflected can boost your credit score. Then, take a look at areas where your credit history is negatively affecting your score. These are the areas to work on. And while every financial situation is unique, here are some things you can do to help improve your score.

Fixing Reporting Errors

Before you get into improving your credit score, it’s important to make sure there are no errors on your credit report. As we mentioned before, take advantage of annualcreditreport.com(opens in a new tab) to get your free annual credit report from each major credit reporting agency—Experian, Equifax, and TransUnion. If you do find errors, contact each agency separately and let them know in writing that the information is inaccurate along with proof of why it’s inaccurate. Then, reach out to the company that misreported the information and do the same. For example, if it’s a credit card company reporting a late payment that wasn’t late, get in touch with them in writing about the error and make sure they remove this from the report.

Pay Bills on Time

One of the biggest contributors to your credit score is on-time payments. If you’ve made late payments or missed payments in the past, these are hard to fix and could cause late fees. Late payments typically start getting reported to credit reporting agencies when payments are 30 to 90+ days past due. As an example of how to avoid this, set up payments so they are automatically deducted from your bank account when they’re due. The best thing you can do going forward is to get payments in on time and know that past credit problems may have less of an impact on your credit score as time moves on.

Pay Down Debt

Paying off debt, especially credit card debt, can make a big difference in your credit score. It’ll increase your available credit and help lower your debt-to-income ratio. There are different ways to go about paying off debt, like paying more than the minimum monthly payment, reducing or halting credit card spending, creating a budget, using only cash to make purchases, and paying off your most expensive debt first. These are just some suggestions. Be sure to do your research to find the approach that works best for you. You can also check with a housing counselor who can help guide you with personalized recommendations based on your goals.

The Consumer Financial Protection Bureau (CFPB) provides an online tool where you can search for housing counselors in your area. These counselors are approved by the U.S. Department of Housing and Urban Development (HUD).

Avoid Opening New Accounts

If you’re trying to improve your credit score, avoid opening new credit card accounts. This can negatively impact your score for many reasons, including the risk of taking on more debt and lowering your average account age. It also increases the number of inquiries to your credit report, which can affect your score.

With that said, do not close accounts you already have open. These existing lines of credit can help with factors like average account age (the older the better) and how much available credit you have.

Establishing Credit (Before applying for Mortgage)

If you haven’t begun establishing credit through credit cards, loans, or other bills, you’ll want to start right away, only take these actions before applying for a mortgage unless the Lender asks you to. Most lenders need to see that you can make payments on time and responsibly manage credit. This lesson offers a few ways to start building up your credit.

Open Accounts

The first thing you can do before starting to build up your credit is to open a checking account or savings account if you have not already done so. Mortgage lenders will most likely require this information on applications as it helps document your source of funds for a down payment. Also, if you open a credit card or other credit-establishing account, it’s usually easier to pay bills and make other financial transactions through your checking account.

Use Credit Cards Responsibly

When used properly, credit cards are a great way to build up or improve your credit report. If you don’t have a credit card yet, you could try applying for one from a retailer or applying for a secured card from a bank. (A secured card requires a security deposit.) Both of these options usually have lower balance limits and higher interest rates. Then, after a year of establishing some credit, you could try to apply for an unsecured card from a major financial institution to replace a store card or secured card.

The thing with credit cards, though, is that it’s important to avoid using the full amount made available to you. You should aim to pay the balance in full each month so that you do not carry a balance from one month to the next.

Make sure to charge only what you can afford to pay in full, on time. If you carry a balance, you’ll end up paying interest on that purchase, which could cost you way more than the original purchase price. This will negatively affect your credit score. As credit card debt builds up, it becomes harder and harder to pay off.

Pay Bills On Time

This is probably one of the most important factors in building credit: paying your rent, loan payments, and other bills on time. For revolving accounts, it’s very important to pay at least the minimum payments, but you should aim to pay the balance amount in full each month. Revolving accounts are credit arrangements that require you to make periodic payments but do not require full repayment by a specified point of time.

Generally, using 30% or less of available credit is favorable and will be an important factor when lenders determine if they’re willing to lend you money. If you’re paying off student loans, it’s extremely important to avoid defaulting, as it can take years for your credit score to recover.

Resources

Here are some helpful resources from this module, plus others which you’ll find useful during your homebuying journey.

Fair Credit Reporting Act (FCRA) Website

You can get three free credit reports a year—one from each credit reporting agency at annualcreditreport.com(opens in a new tab). VIEW WEBSITE

Affordability Calculator

How much home can you afford? This calculator can help you estimate this based on factors like your income, debt, and how much you want to put down. VIEW CALCULATOR

Mortgage Calculator

This calculator can help you figure out an estimate for monthly mortgage payments based on factors like home price, loan terms, and how much you put down. VIEW CALCULATOR

Homebuying Glossary

This glossary contains common terms often used in the homebuying process and their definitions. VIEW GLOSSARY

Down Payment Assistance Resources

Use this website to find resources to help with your down payment. FIND RESOURCES

HUD-Approved Housing Counseling Agencies

This website lets you search for HUD (U.S. Department of Housing and Urban Development) approved agencies by zip code. FIND A COUNSELOR

More First Time Home Buyer Info:

+ Rent or Buy.

+ Shopping with a Lone Star Luxury Agent.

+ Finding a Lender.

+ Understanding Debt.

+ Things To Consider Before Buying.

+ Understanding the Mortgage Loan Process.

+ Basic Types of Mortgage Loans and Terms.

+ Looking at Types of Homes.

+ Submit a Home Offer, Get an Inspection.

+ Closing your Loan.

+ Welcome to Homeownership.